“Nothing very bad can happen to you there” — said Holly Golightly, the main character of The Breakfast at Tiffany’s novel by Truman Capote. Holly, of course, meant Tiffany’s & Co. store at the 5th avenue in New York city. A beautiful place with tons of stylish and luxurious jewelry does make the impression that nothing bad will ever occur to you there.

The same thing can’t be said about mobile banking app development. Moreover, a very small number of neo banks succeed today, so your future journey will probably not look like the breakfast at Tiffany’s — more like a dinner in hell.

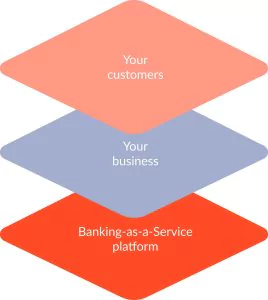

But it doesn’t have to stop you from building a banking app. Thanks to the Banking-as-a-Service (BaaS) model, you’ll be able to reduce development costs dramatically and avoid much pain related to connecting your product to banks, regulations compliance, securing customer data, and so on. The JatApp team has been developing fintech products since 2015, and we know what challenges fintech companies need to overcome before they make a confident stride over the market. For that reason, we’re going to pin down the concept of BaaS and explain how it can help save your resources on developing your banking app.

Just another something-as-a-service?

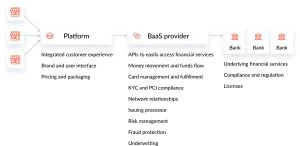

Exactly. But this time, it’s about banking and everything related to it. Let’s take a look at a simple example. Fintech startups rarely have access to banking infrastructure that involves connections with community banks, clients’ bank accounts, payment systems, security measures, application programming interfaces (APIs), frameworks for regulations’ adherence, to name a few.

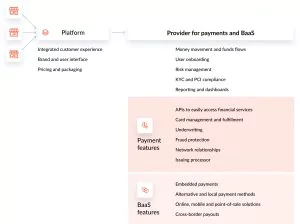

Instead, fintechs look for BaaS companies that can connect them to all those things and even manage regulatory compliance on their behalf. In such a way, BaaS is a company that provides fintechs and non-financial businesses with access to banking services and a relatable ecosystem of the financial sector.

There are different types of BaaS that serve different purposes:

- Card issuing and account management

- Agency banking

- Core banking services

- Lending and mortgage banking

- Product management

- All of the above combined

BaaS does all the grunt work for you. You just have to pay for a subscription or a percentage fee from each transaction completed with your banking app.

We can bet that every fintech entrepreneur dreams about a bank-in-a-box ready for use, which is why the tremendous growth of BaaS is easy to explain. Gartner reports that BaaS will see a mainstream adoption in one to two years to come, while nearly 30% of big incumbent banks will launch their own BaaS solutions by 2024. The Universe does have a sense of humor: incumbent banks will spend money on helping you compete against them in the future.

On a side note, we have one more thing to discuss in relation to BaaS definition. We would like you to pay attention to the difference between BaaS, open banking, and platform banking.

- Open banking provides non-financial businesses with banking data through APIs to make payments and gather different consumer insights.

- Platform banking is an advanced form of open banking that enables banks to provide a range of services (fintech-related usually) from third-party companies in order to advance customer experiences.

- BaaS are licensed banks that offer infrastructure, regulations, and core banking services to fintechs/other businesses, thereby integrating the entire banking system into their products.

What BaaS can do for your banking app

Banking-as-a-Service looks like a blessing to your banking app, and sounds too good to be true. “Hey JatApp, aren’t you sugarcoating BaaS?” — you may ask. We have nothing to hide, just take a look at the advantages BaaS offer and you’ll see why this kind of service is ballooning that high today:

- Connecting to banks and their infrastructure. We’ve already said that fintechs seldom have their own banking infrastructure and what’s more important, license. That’s why BaaS companies offer to take a bureaucratic burden off the fintechs shoulders. With BaaS, you’ll have plenty of time to focus on your product rather than doing tons of paperwork.

- Core banking services. You connect to BaaS, and your banking app will be able to process your first customers right away. The speed of bringing a product to market is a little lower than Elon Musk’s mood swings.

- Access to a wider customer base. Startups, especially fintech ones, always have a struggle of gathering a customer base big enough to generate revenue for further growth. Many BaaS, like Treasury Prime, work as matchmakers between startups and large incumbent banks. Treasury Prime, by the way, managed to connect more than 100 fintech startups to mainstream banks for the last year. By having connections with a big incumbent bank you have better chances to get recognized. On top of that, some BaaS can set up a date with an incumbent, and you’ll discuss the terms of your app promotion within the incumbent customer base. In the same vein, BaaS can be a good matchmaker with similar fintechs that search for a partnership with banking app startups like yours.

- Compliance with regulatory requirements. Again, we’ve mentioned this advantage several times already, but we can’t stress enough the value BaaS is able to bring to your banking app project by managing all legal issues for you. You can keep developing your product, while your licensed BaaS provider keeps an eye on the cleanliness of the banking’s regulatory side.

- Linking to non-financial products and services. Many businesses, especially Software-as-a-Service ones, look for integrations not only with big incumbent banks, but also mobile banking apps to advance the experiences of their own customers. Actually, BaaS can serve a purpose of a marketplace, where you find customers, fintech partners, and even new product areas to penetrate to.

And boom! All these benefits can result in the 95% cost savings in customer acquisition that is one of the main hurdles for banking app startups today. We drop the microphone with that swag feedback sound.

However, it doesn’t necessarily mean you have to run to the first BaaS bank you can find and sign the agreement. Think about exact services they offer and compare their benefits with gaps/pains you’re facing. We don’t recommend you going to such popular BaaS like Solarisbank, Starling Bank, or BBVA just because they’re some sort of mainstreamers. They may be just not your cup of tea, because you look for other needs being covered.

That is why, don’t let your BaaS shape the value offer you’re going to present to your target audience. Instead, keep looking for a BaaS that will be an enabler of your capabilities rather than their determinant.

And one more thing. Not all fintechs are ready for adopting BaaS. Make sure your whole team has an open mind and understanding of benefits BaaS can bring. Use the image below as a checklist.

What BaaS cannot do for your banking app, but JatApp can

…create it. Our company has experience in developing various fintech products like payment gateway, personal finance app, and payroll solution, so we can help you with mobile banking application development. In fact, 99% of our clients leave positive feedback about the products we developed for them. You can expect a solution of high quality and totally aligned with your business goals.

If you want to develop a banking app that is nice and elegant like Tiffany’s & Co. jewelry while meeting real business requirements, leave us a note. We’ll reach out to you as soon as possible.